Q1’2026 Update: Navigating a Stable Consumer Confidence Landscape

Welcome to Malaysians on Malaysia (MOM): Oppotus’ quarterly report that provides in-depth insights into the Malaysian Consumer Confidence Index (MYCI). It is an ongoing effort to offer insights into Malaysia’s evolving market landscape. This edition delves deeper into the latest consumer trends and key influencing factors, including financial outlook, economic confidence, digital payments, tech trends and more, offering a fresh perspective for strategic decision-making. Join us as we explore the driving forces behind this quarter and the potential implications.

Moving into the year 2026, consumers’ confidence continues to remain stable in the first quarter. This stability was likely due to the two major festive seasons falling in the same quarter; February celebrates Chinese New Year, while March celebrates Hari Raya Aidliftri. Towards the end of the quarter, it was concerning as the global energy impact was the talk of the town due to the geopolitical impact. Before we dive deeper into this chapter, readers are encouraged to revisit the Q4 2025 MOM report.

Malaysians’ Confidence Holds Firm

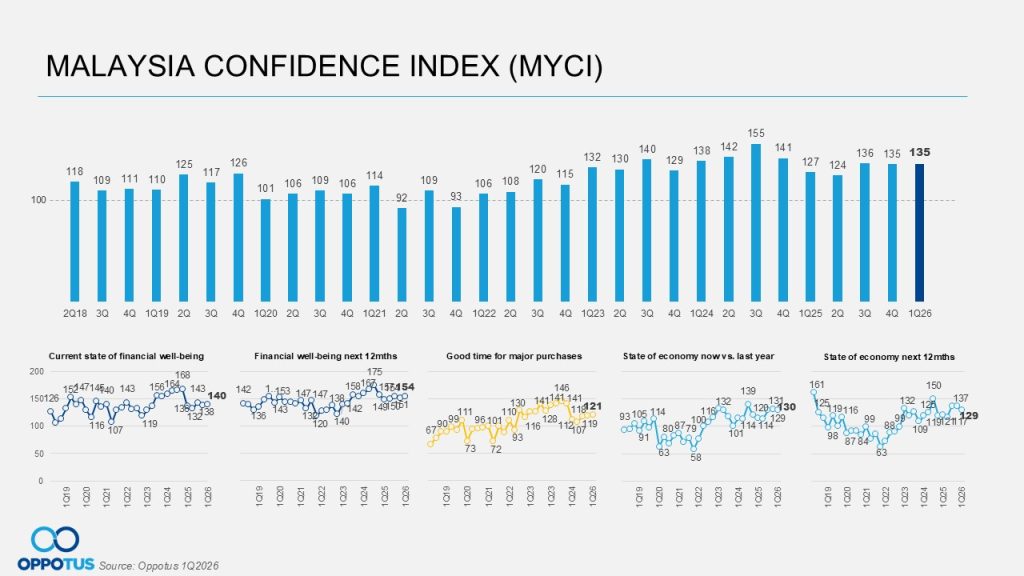

Malaysians start the year 2026 with a flat consumer confidence at 135 points. SARA aid of RM100 was given starting early February for all Malaysians in preparation for the upcoming festive season. This contributed to a stronger 5.4% GDP at the start of the year, driven by domestic demand.

Economic Sentiments Remain Flat

Economic growth remained flat in the first quarter of 2026 at 130 points, which is just one point lower than the previous quarter. While year-on-year figures improve by 15 points vis-a-vis “Q1 2025”’s 115 points. The vulnerability of oil prices and supply due to the geopolitical tension in end February has led the government to announce the adjustment to the monthly fuel subsidy under the Budi95 scheme from 300 litres to 200 litres per month per individual starting from the first of April.

E-Wallets are Part of Daily Essentials

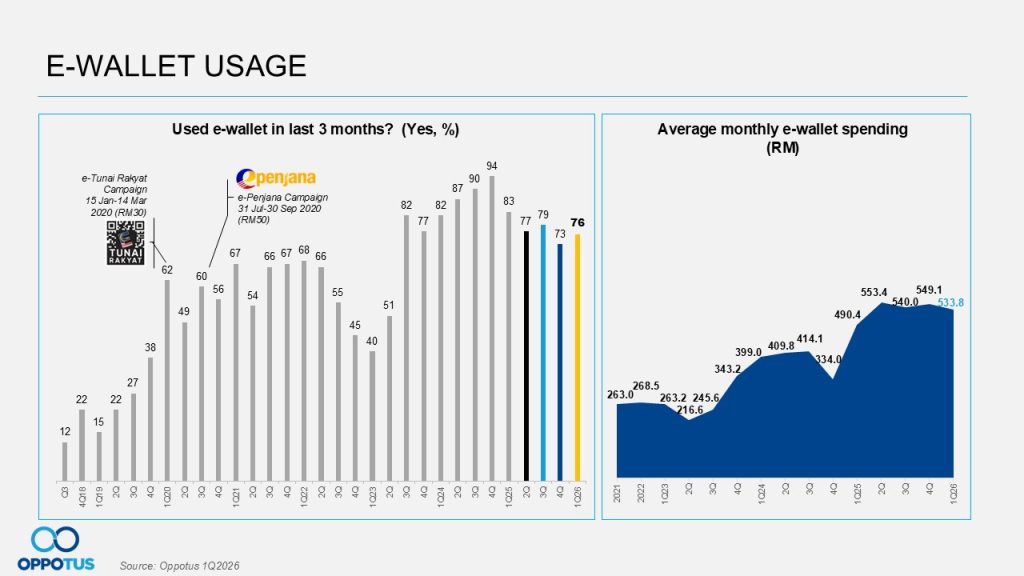

E-wallets have become part of Malaysians’ daily essentials as it continue to hover between 70% – 80% usage since 2025. This is reflected in Q1 2026, at 76% usage rose by 3% from the previous quarter. While looking into the average spend, it continues to stay RM500 and above for four quarters, including quarter one 2026 at RM533.80. Based on Oppotus yearly e-wallet report, e-wallet usage share for physical transactions has surpassed cash by 3%.

If you are eager to dive deeper into these numbers and gain a more nuanced understanding of the forces shaping the future of business and finances, reach out to us at theteam@oppotus.com. You can also hop onto our alternative service, Oppotus DoubleDecker, an Omnibus solution to gain a first-hand preview of our next MOM report.

The start of 2026 see Malaysians settling in on the consumer confidence index at 135 points, which is similar to the previous quarter. Though the stability remains, it has some notable movements on the other MYCI components that will be explained in this article.

This confidence level is among the highest of quarter one since 2018. It was likely to be impacted by the celebration of two major festivals in Malaysia; February Chinese New Year, March Hari Raya Aidilfitri. Due to this celebration, the government has given the RM100 SARA aid to all Malaysians to be received in February.

In early March, the government shared several initiatives announced to ease the cost of living. The key initiatives were to bring forward Sumbangan Tunai Rahmah (STR) payments for 5.2 million recipients, as well as Special Financial Assistance for civil servants, retirees, and veterans, cooking oil subsidy enforcement, flight ticket subsidy and many more. These initiatives proved useful as later in the month, the Department of Statistics Malaysia (DOSM) reported that Malaysia’s inflation rose modestly to 1.4% in February, with the consumer price index (CPI) increasing to 136.0 from 134.1. While about 59.7% of items (342 of 573) recorded price increases, of which 333 items (97.4%) increased by 10% or less, while only 9 items rose by more than 10% in February 2026.

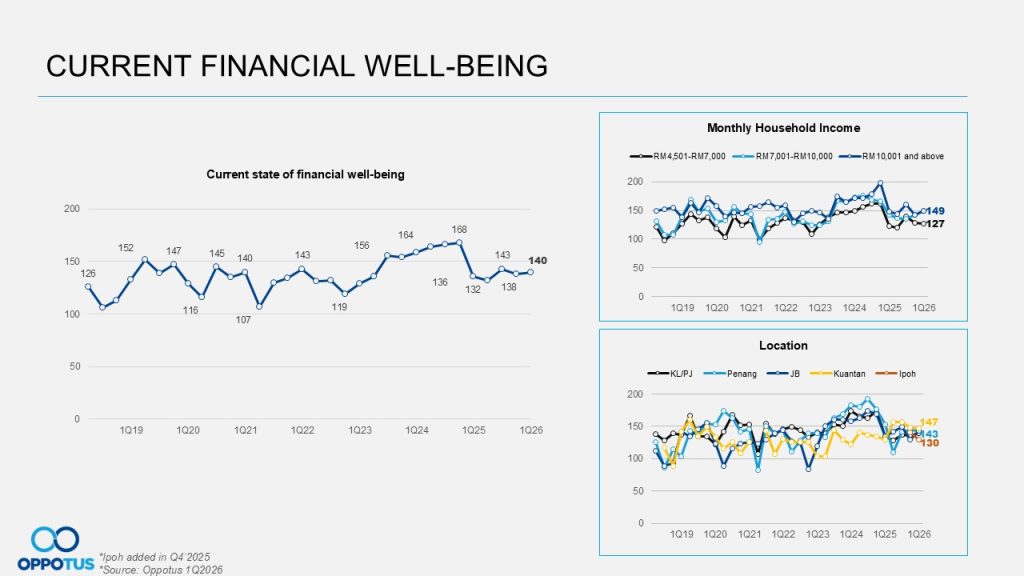

Despite the rise of inflation within the quarter, Malaysians still hold on to the positive outlook of the financial well-being in this quarter. It had a marginal uptick of two points from the previous quarter, resulting in 140 points.

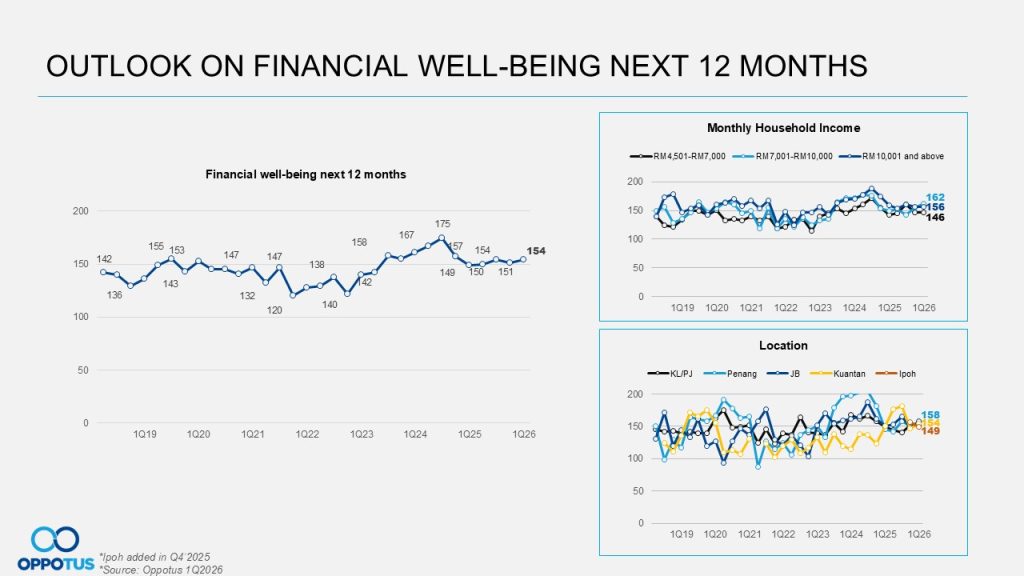

During this quarter, BNM has shared that the rise in headline inflation of 1.6% (Q1 2026) from 1.3% (Q4 2025). It has reflected some initial cost pass-through of higher global cost pressures, partly due to the geopolitical tension in the Middle East. Having such a major event happen, it does not impact Malaysians as much due to the positive initiative for the big festive season given by the government. The inflation pervasiveness, measured by the share of cost per index (CPI) items registering monthly price increases, continued to decline to 38.3% during the quarter (Q4 2025; 39.6%), trending well below the historical first quarter average of 52.2%.

Therefore, the financial well-being of most consumers for the next 12 months appears optimistic. A slight uptick recorded 2% rise, resulting in 154 points in quarter one — this is reflected in the overall key location in Malaysia.

SARA aid is likely to be the main contribution to this uptick in Malaysians’ financial well-being of current and next 12 months. Additionally, toll discounts were offered during the CNY and Raya periods to ease travel back to kampung for commuters.

Aside from the SARA aid, the unemployment rate has held steady at 2.9% with a 1% decrease from the previous quarter. Malaysia’s labour market in the coming months is anticipated to remain favourable, as the unemployment rate remains low, it reflects stronger labour force conditions. The labour force participation rate, the proportion of persons employed or looking for work, edged up to 70.9% in January 2026 from 70.8% in December 2025. This employment rate brings strong financial benefits as it means more Malaysians have financial stability.

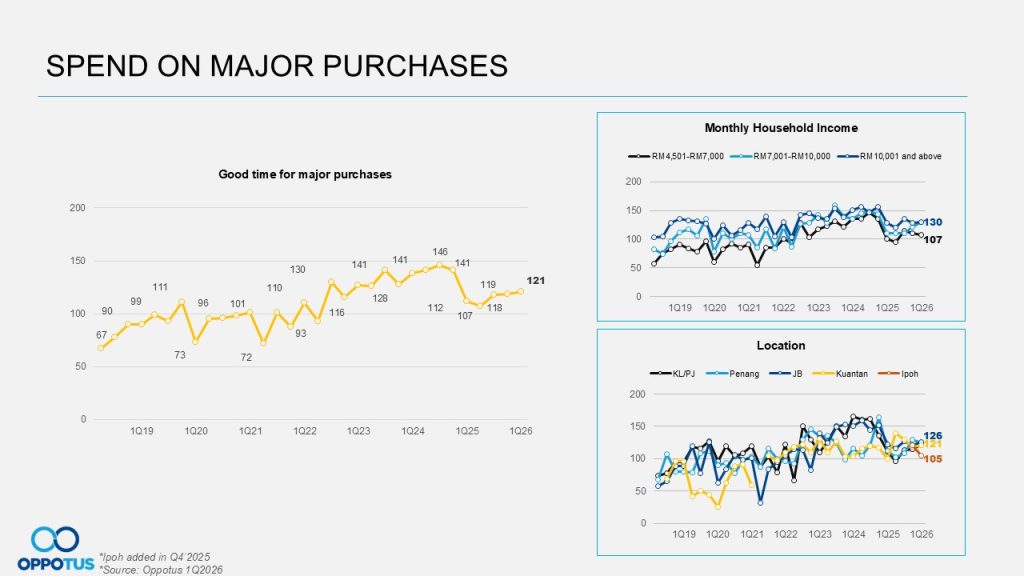

Stability continues into spending on major purchases with a score of 121 points, despite the slight dip in financial well-being. The necessity to spend during that period was higher due to the festive season. As such, e-commerce took the opportunity to engage and promote by using the festive season as a theme.

Shopee took the opportunity of 2.2 Double Double Sales to reward shoppers, covering daily essentials to fashion, food, and gadgets by giving out limited-time deals and surprise voucher drops. Moreover, it delivers exclusive RM10 and RM100 Knockout Deals. This campaign was then followed by Ramadan deals. Not to forget, TikTok launches “Super Season” campaign positions Malaysia’s 60-day festive convergence. They also assist enterprises to tap into the 2026 convergence. TikTok introduced Festive and Holy Month packages, including TopView Boost, Scripted Series and Branded Search Hub.

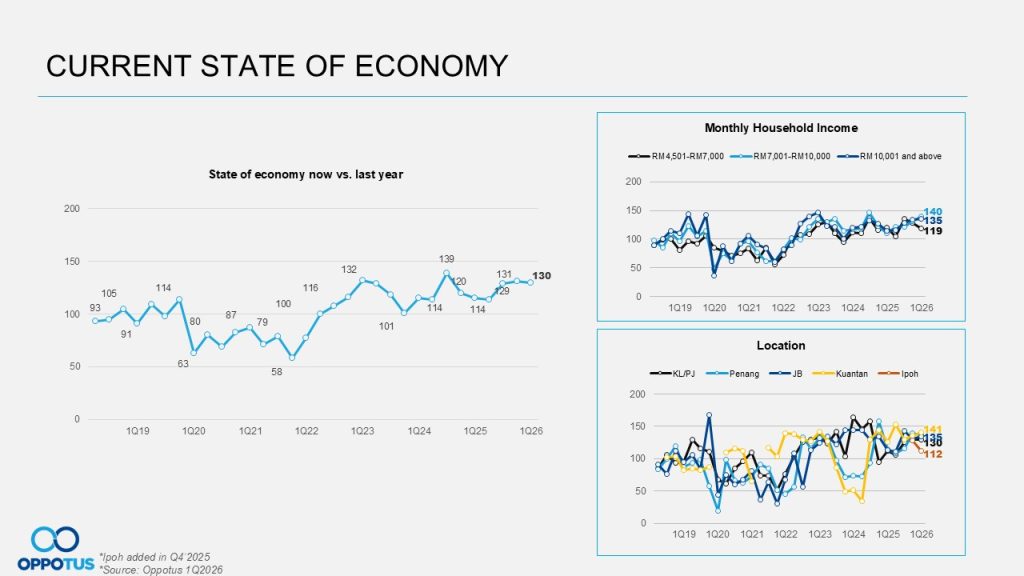

The current economy remains optimistic, carrying a 1-point contraction from the previous quarter, resulting in a 130 points versus 131 points in Q4 2025. Zooming into year-on-year, it rose 13% from Q1 2025 (115 points). Such results were also reflected in the gross domestic product (GDP), as it rose 25% with a result of 5.4% (Q1 2025: 4.4% GDP).

On top of that, Tourism Malaysia has made an effort in that quarter to lure tourists to Visit Malaysia and boost our economy. This quarter has hit a record high with international visitor arrivals rising 5.4% year-on-year to a record 10.65 million. This record is driven by Chinese New Year travel demand and expanded flight connectivity. China remained the largest growth contributor with more than 280,000 visitors or 25.2% year-on-year.

As a whole, Malaysia’s economy still remains at a positive tone even though the global narrative is otherwise due to geopolitical factors impacting global energy prices. The vulnerability of oil prices and supply started at the end of February 2026 – it has led to government measures by adjusting the monthly fuel subsidy under the Budi95 scheme from 300 litres to 200 litres per month per individual starting from the first of April.

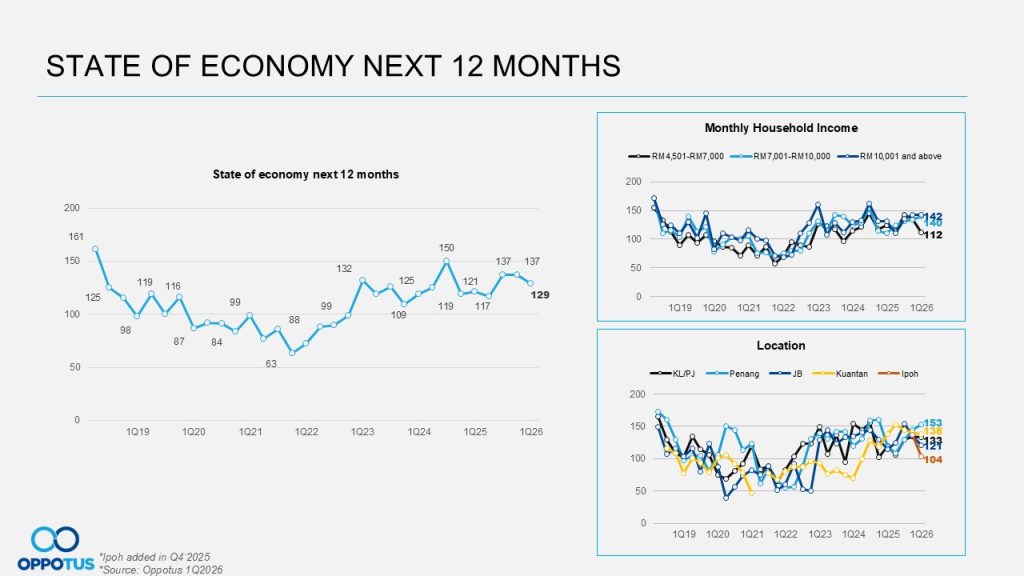

In spite of the positive tone on the current economic situation, Malaysians are much more worried about the upcoming 12-month economic outlook. A concerning gap is seen as it fell 6% from the previous quarter (from 137 points to 129 points).

The global uncertainties are one of the major causes of economic confidence, which also potentially leads to a higher cost of living. M40 group is embracing and worries as much as it has the highest dip from 136 points in Q4 2025 to 112 points in Q1 2026, in line with the current headline inflation that rose by 0.2%. Based on BNM’s report, electricity charges and fuel prices, mainly RON97 and diesel, increased during the quarter, which led to slower declines in electricity (-6%; 4Q 2025: -10.3%) and fuel inflation (-1.5%; 4Q 2025: -1.9%).

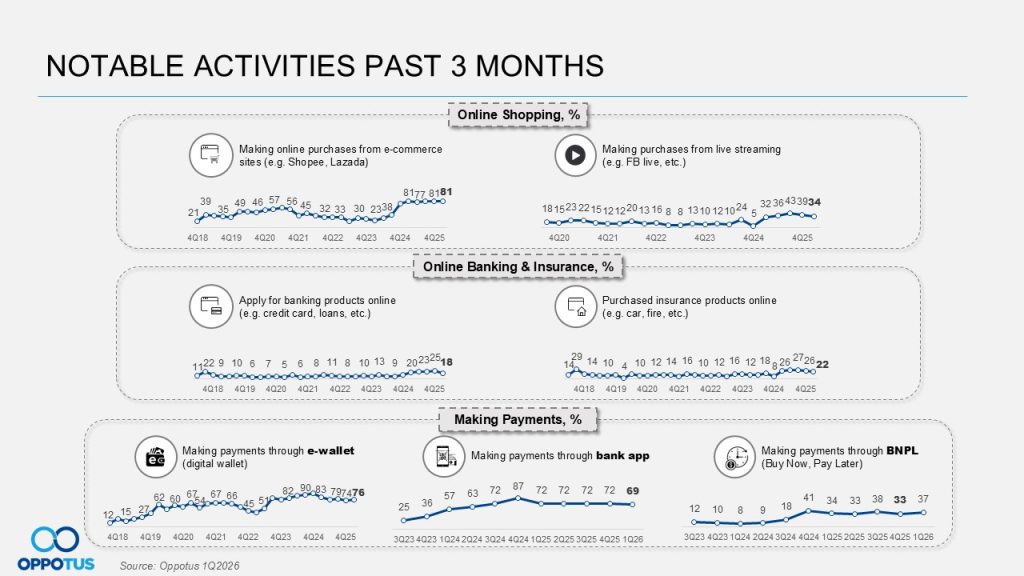

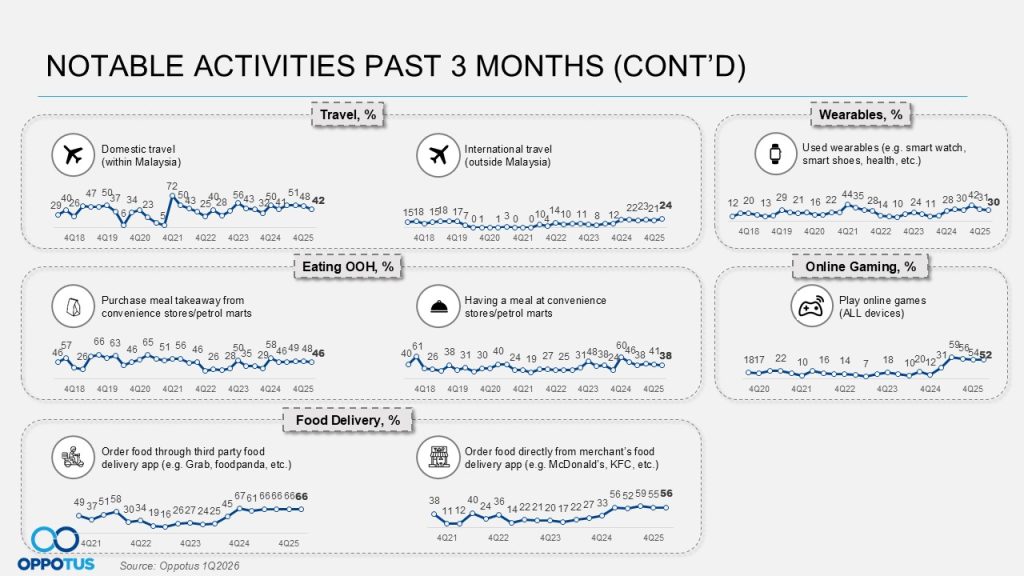

Therefore, most of the activities in the past 3 months remain stable and/marginal uptick. It can be seen in Online Shopping, as when it comes to making online purchases from e-commerce sites, it remains stable at 81%. While making purchases from livestreams, a decline of 5% was seen (from 39% to 34%). During this period was expected to see a higher spike in purchases due to the multiple campaigns for CNY and Raya, but the results say otherwise.

Food Delivery were also seen to remain plateaued, especially ordering through third-party food delivery apps (Grab, Foodpanda, etc.). This is because it has been scoring 60% – 67% since Q 2024. Ordering food directly from the respective merchant’s food delivery apps also hovers within 50% since Q1 2025 till now. The convenience of food delivery trend does not seem to be surpassing the trend, as consumers still have the preference of dining in and taking away directly from the restaurant itself. In a similar topic, Eating Out-of-Home (OOH) is seeing a slight decline from the previous quarter for both having purchasing a takeaway meal from convenience stores or having a meal there. Both decline between 1% and 3% respectively.

Moving into the technology activities, Wearables continue to dip since the last quarter. Q4 2025 has scored 42% as the highest since 2022, but it continues to dip to 30% in Q1 2026. This trend is continued into Online Gaming as well, scoring a high 59% in Q2 2025 and slowly dropping to 56%, 54% and now 52% in Q1 2026. Possibility of the economic downshift alongside headline inflation contributes to the consumer’s financial priority, as both wearables and online gaming are good-to-have items.

Shifting the narrative to e-wallet landscape, which became Malaysians’ daily essentials as it continues to hover between 70% – 80% usage since 2025. In Q1 2026, the usage rose by 3% from the previous quarter – resulting to 76%. As such, this confidence has brought the average monthly spend to be much more positive. It also started to hover within RM500 per month since Q2 2025, including Q1 2026 at an average of RM533.80. Based on Oppotus yearly e-wallet report, e-wallet usage share for physical transactions has surpassed cash by 3%.

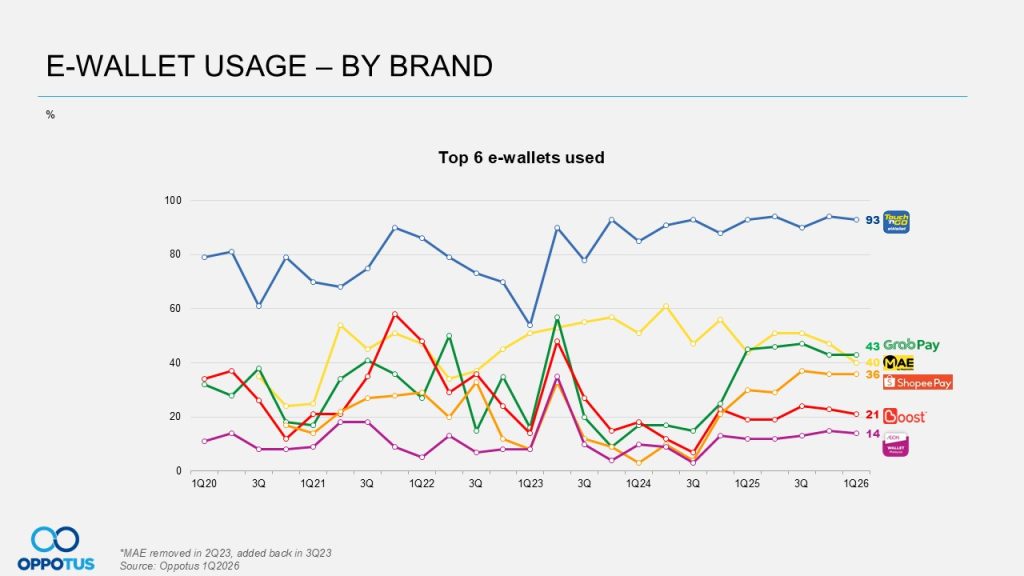

Majority of e-wallet usage by brand did not have a heavy impact on increasing usage, including the e-wallet leader Touch n’ Go, which holds firm to its position at 93% usage. While GrabPay and ShopeePay still hold on to the usage percentage from Q4 2025, 43% usage and 36%, respectively.

MAE position has shown a 7% decline to 3rd place by scoring 40% usage, resulting in GrabPay taking over the second position in quarter one. The last downfall of the second position was in Q2 2023, scoring 4% lower than GrabPay. All-in-all the highest gap was during Q2 2022, with a 16% decline from GrabPay.

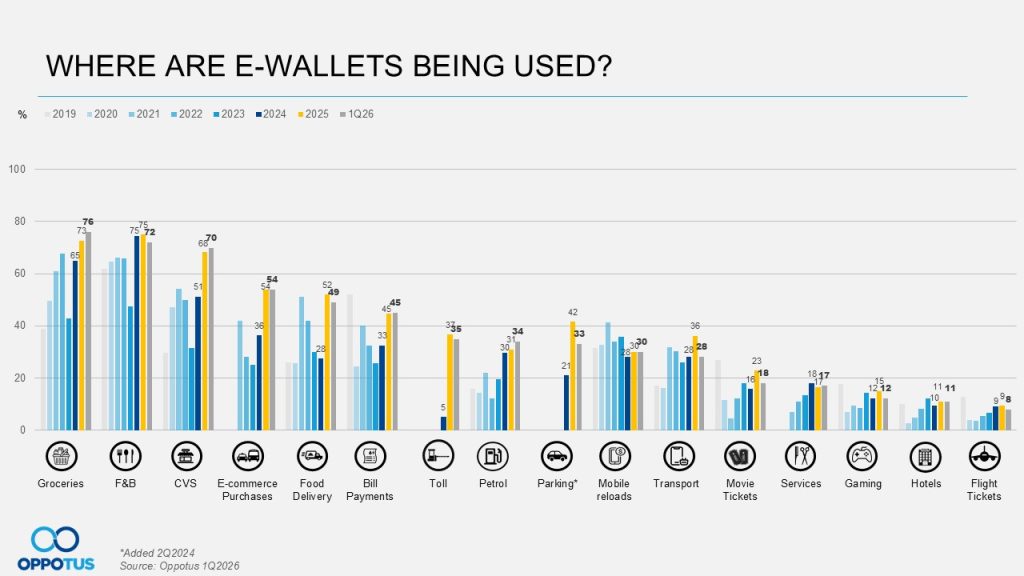

Zooming into the e-wallets usage category, it has been established that the top 3 are F&B, Groceries, and Convenience Store (CVS) in no particular order. In Q1 2026, the Groceries category started the year strong at 76% usage, followed by F&B at 72%, then CVS 70%. Groceries being the top used make sense due to it being a festive season, supermarkets/hypermarkets took advantage of this, such as Village Groce ran a promotion “Fresh Pick for A Prosperous New Year” alongside giving out festive gifts, pre-order CNY cookies, canvas bag, angpao and many more. AEON Retail too kick off the year with “Everyday Fresh, Everyday Low Price deals” by providing discounts/package prices during this period.

While Food Delivery has also taken over the spot of Bill Payment by landing in fifth place, 49% usage. The food-related and vehicle category sees a slight increase due to the festive season, where people tend to feast and travel by vehicle much more. Hence, Tol and Petrol remain the mid-category tier with minimal adjustments at 35% and 34% usage.

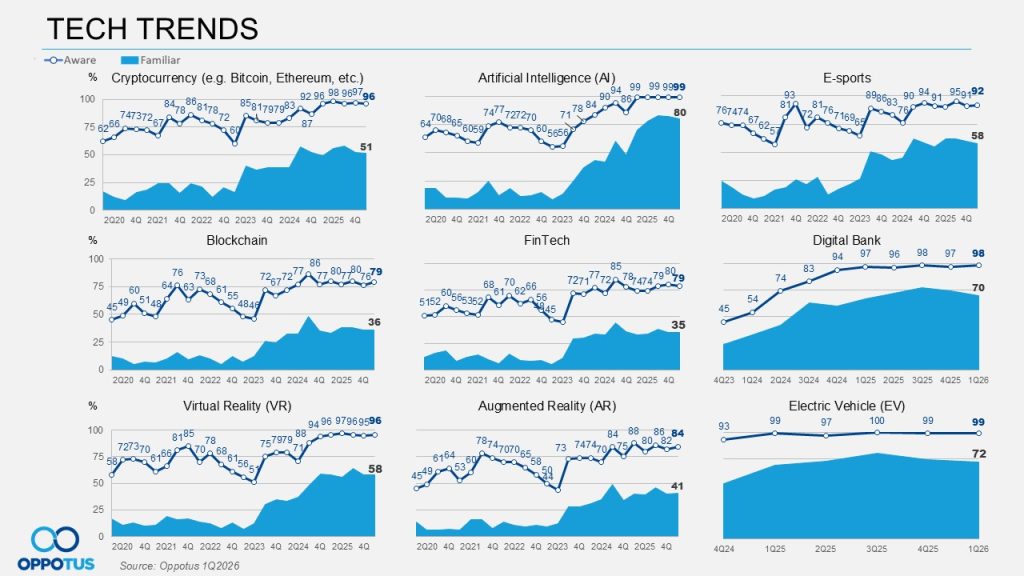

Switching into Tech Trends, which the government encourages most Malaysians and companies towards digital implementation, since Malaysia is targeted to be digital and AI-savvy. Therefore, AI awareness remains at an all-time high at 99% and a 80% familiarity. It is aligned with the government’s expectation of an AI-standards framework to show clear progress within the next 12 months, marking a key step towards positioning as an “AI nation” by 2030. The framework consists of 3 components, namely standards development, regulation and compliance, and legislation and enforcement.

That said, Augmented Reality (AR) also saw an increase in Q1 2026, with 84% awareness and 41% familiarity (both rose between 1 – 2%). During this period, MCMC secured a major award for its MetaHRise platform – build based on an AR and VR system to completely revamp its corporate onboarding. This initiative reduced employment onboarding by 40% and boosted internal role clarity from 48% to 83%. Additional development phases include deeper functional simulations, virtual division tours, and structured leadership engagement environments.

One of the categories in Tech Trend, the Blockchain, has the best performance as both awareness and familiarity have increased at 79% and 36% respectively. This increment may be contributed by Bank Negara Malaysia (BNM)’s announcement of the Digital Asset Innovation Hub (DAIH) onboarded with 3 initiatives to test real-world application involving ringgit stablecoins and tokenised deposits in 2026.

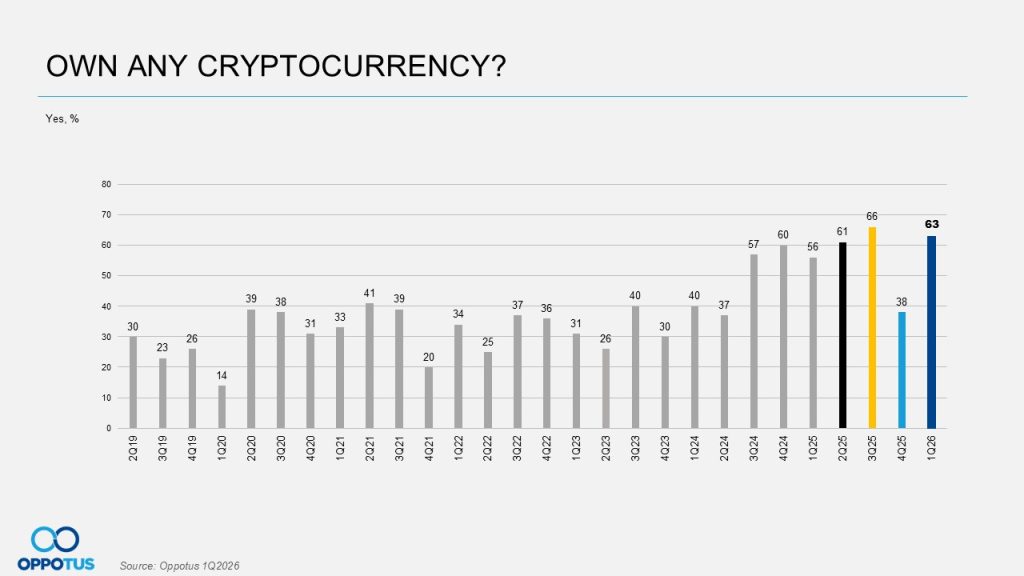

Moving into Cryptocurrency, which has regained its ownership, as the past quarter (Q4 2025) had a huge downfall. Now it is stabilising within the average of 60% ownership, resulting at 63% in Q1 2026. At some point, cryptocurrency market has shown a reduced sensitivity to both good and bad news — a sign of a market searching for its footing.

Cryptocurrency market is also expected to reach an all-time high this year, according to Ripple CEO. As of October 2025, Bitcoin has seen an all-time high of $126,000, and there are “major” financial institutions showing interest in crypto, which is a “massive sea change”.

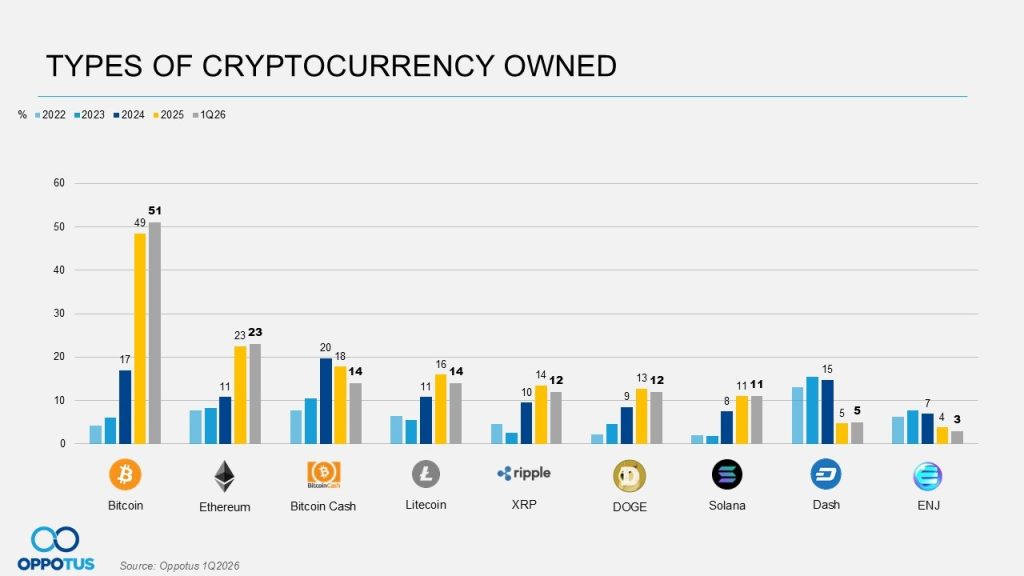

The positive increment of cryptocurrency ownership has automatically impacted the type of cryptocurrency owned. Bitcoin has a major impact, as in Q1 2026 alone has surpassed the average in 2025. As results Bitcoin ownership in Q1 2026 is at 51%, a 2% increase from the average in 2025.

While Ethereum resulted 23% ownership, which is similar to the average of 2025 in total. This similar result is reflected in Solana and Dash currencies, respectively, which owned 11% and 5%.

Oppotus stays committed to acquiring insights through continual analysis, offering a unique perspective on the country’s trends and consumer landscape.

Note that the opinions presented regarding Malaysia and its people reflect the views of Malaysian citizens aged 18 and above, from all income segments, residing in key cities of the Peninsular, and selected in a representative manner.

For a more granular analysis of the data above, contact us at theteam@oppotus.com. Our team of experts would be pleased to facilitate a comprehensive review and offer customised recommendations tailored to your needs. Alternatively, explore the omnibus solution to incorporate additional measures for your business through our MOM study.