CASHLESS RISE IN 2025: E-WALLETS LEAD THE WAY AS DIGITAL BANKS BUILD TRUST AND TRACTION

E-wallets and digital banks – two big segments of players in the financial and commercial landscape of Malaysia with an increasing influence as more and more commercial activities and transactions shift to digital platforms, and more consumers make the transition to a primarily cashless lifestyle – preferring convenience and speed over traditional methods of payment.

While e-wallets have been around for a while and their benefits are well-known at this point, digital banks are a newer concept which have yet to be adopted by Malaysians to the same extent as e-wallets. For those who do make the leap to digital banks, the benefits are numerous. On the whole, digital banks operate without physical branches which means that all transactions and procedures can be handled online, bringing an unprecedented level of convenience to banking. As such, these banks also enjoy lower operating costs which they can pass on as a benefit to customers in the form of perks such as cashback and higher interest rates. A well-known example is GX Bank which at one point offered 1% cashback on all local transactions for Malaysians, leading to many new users joining them to take advantage of this perk. Although this cashback policy now only applies to overseas spending, GX Bank still remains the most popular digital bank in Malaysia, showing that such perks are effective in drawing in new users.

With this in mind, how are the e-wallet and digital bank landscapes shaping up in Malaysia? We took a dive into the details to see how Malaysians are utilising e-wallets and digital banks, and what possible factors could be promoting or hindering the growth of digital banks in Malaysia.

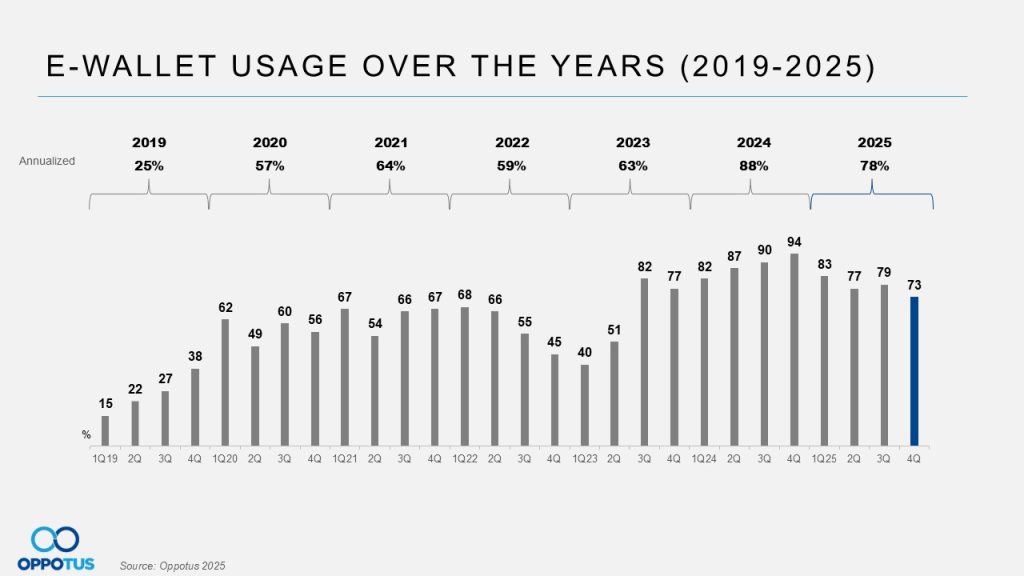

Over the past few years, e-wallet usage has increased overall since they were first introduced pre-COVID. The COVID years then saw an increase in the usage of e-wallets, both due to the preference for contactless payments and the new functionalities of e-wallets, with e-wallet usage now hovering around 70-80% as of 2025. The overall usage of e-wallets in 2025 was slightly lower than the peak year in 2024, but still higher than any of the previous years so far.

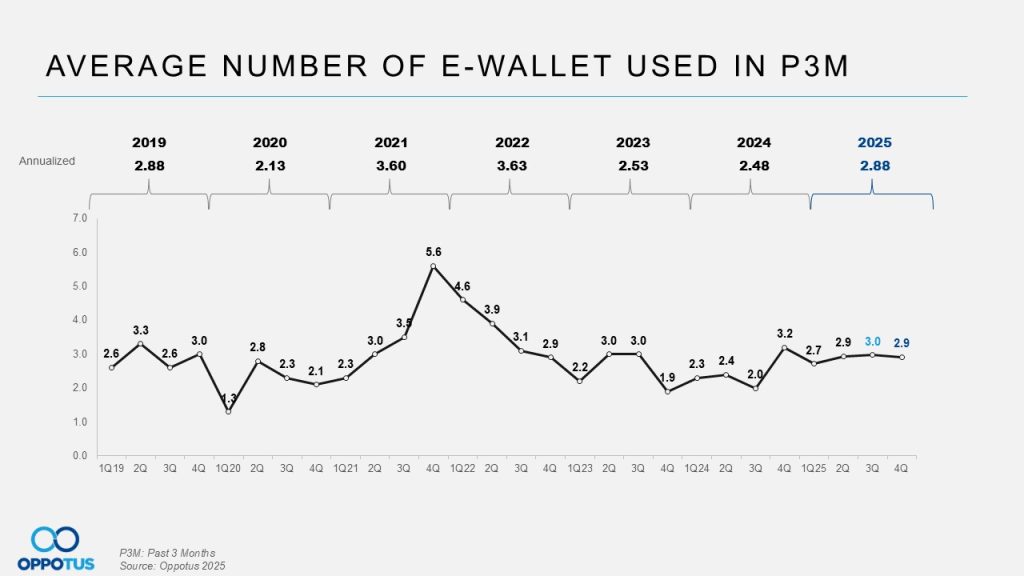

When it comes to the average number of e-wallets that users have utilised in the past 3 months, we see that the number has been hovering around 2.5 – 3.0 e-wallets per user over the past few years. The number of different e-wallets used peaked at 5.6 towards the end of 2021, but that number soon dropped to 3.1 by 3Q 2022 and has stayed around the 2 – 3 range ever since.

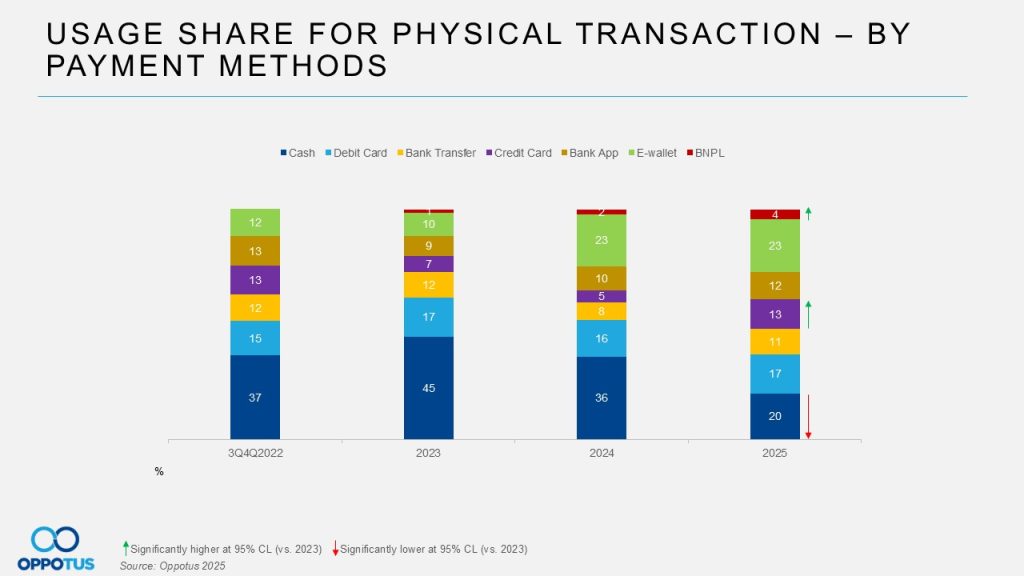

One of the most notable developments in e-wallet usage is its usage share compared to different payment methods when it comes to physical transactions. After having doubled in usage share from 2023, e-wallet usage continues to hold strong at 23% in 2025, overtaking cash as the most used payment method for physical transactions.

Besides e-wallet’s new position as the leading payment method and the significant reduction in the usage of cash, credit cards and BNPL (Buy Now Pay Later) have experienced significantly higher usage compared to previous years, reflecting a general move towards cashless transactions for consumers.

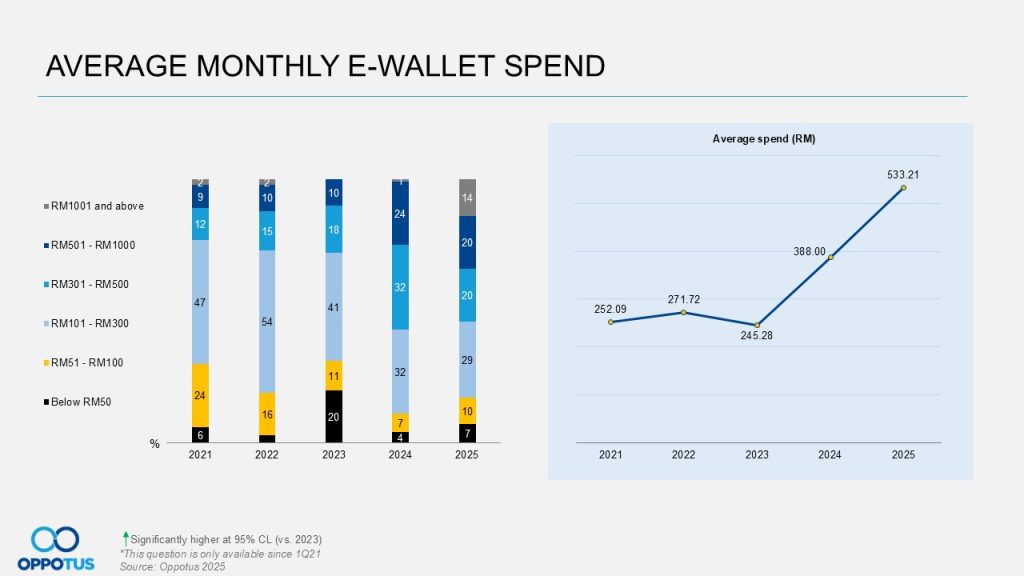

When it comes to monthly spending through e-wallets, we see that the average amount spent by e-wallet users per month has seen a consistent and significant increase from 2023 to 2025. Furthermore, in previous years, we only saw a maximum of 2% of users spending over RM1,000 via e-wallet whereas in 2025, we see that a whopping 14% of users are now spending over RM1,000 every month via e-wallet. Not only does this show that overall e-wallet usage has increased, but that an increasing number of users are willing to utilise e-wallets as a major source of spending/payment option for a large portion of their monthly transactions.

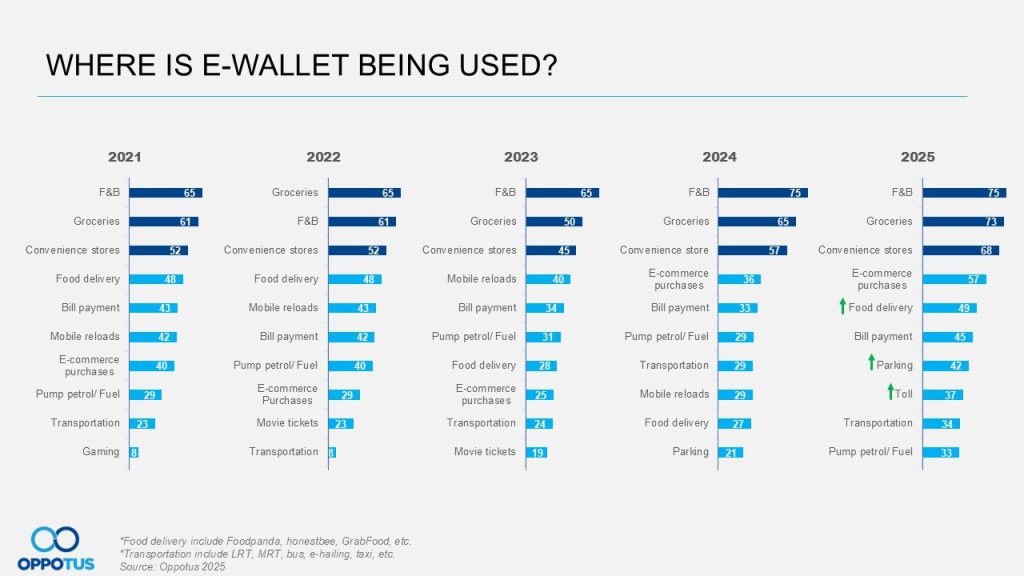

As for where e-wallets are most frequently used, we see that F&B, Groceries and Convenience Stores remain as the top 3 categories for e-wallet usage, maintaining the same position since all the way back in 2021. Also notable is the big jump in usage for 3 other categories in particular: Food Delivery, Parking and Tolls. With parking and tolls being two particular pain points that Malaysian’s struggle with on a daily basis as part of our urban lifestyle, it makes sense that more citizens are turning towards e-wallets as an efficient and convenient way of navigating the obstacles of their daily commute. Meanwhile, the rise of e-wallet usage for food delivery payment could be due to the partnership of GX Bank with Grab, which offers bonus rewards for users who link their GX Bank account to the Grab app.

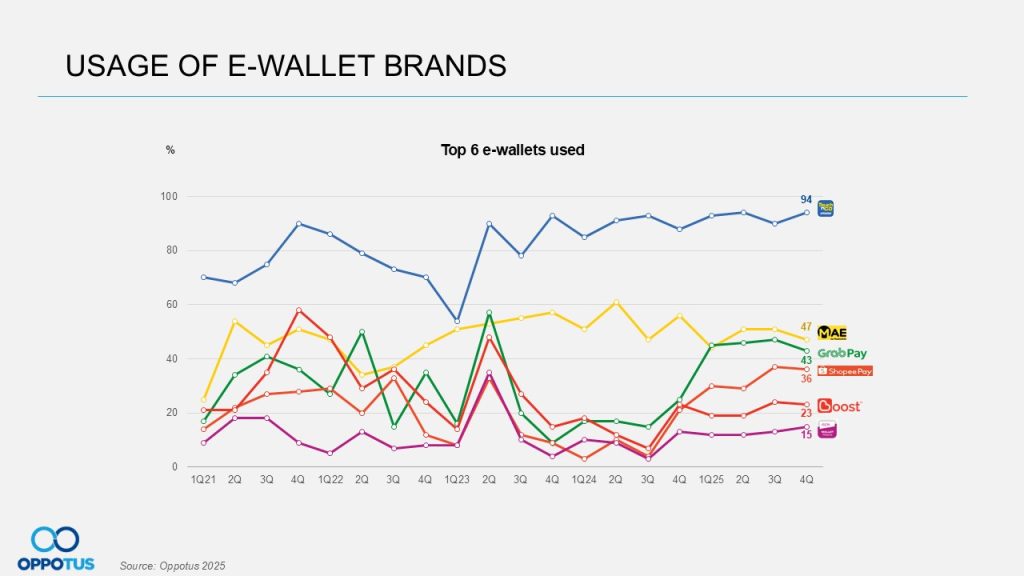

Moving on to our current top 6 e-wallets, we see that the Touch N Go e-wallet is currently the most popular by far, being used by 94% of e-wallet users. The Maybank e-wallet MAE comes in second at 47% usage, followed closely by GrabPay at 43% usage. Another significant development is that BigPay is no longer among the top 6 e-wallets despite having a solid presence in previous years, now overtaken by the Aeon e-wallet as of 2025.

Zooming into the digital banks in Malaysia, they are somewhat newer ground compared to e-wallets which have already been around since the pre-COVID days.

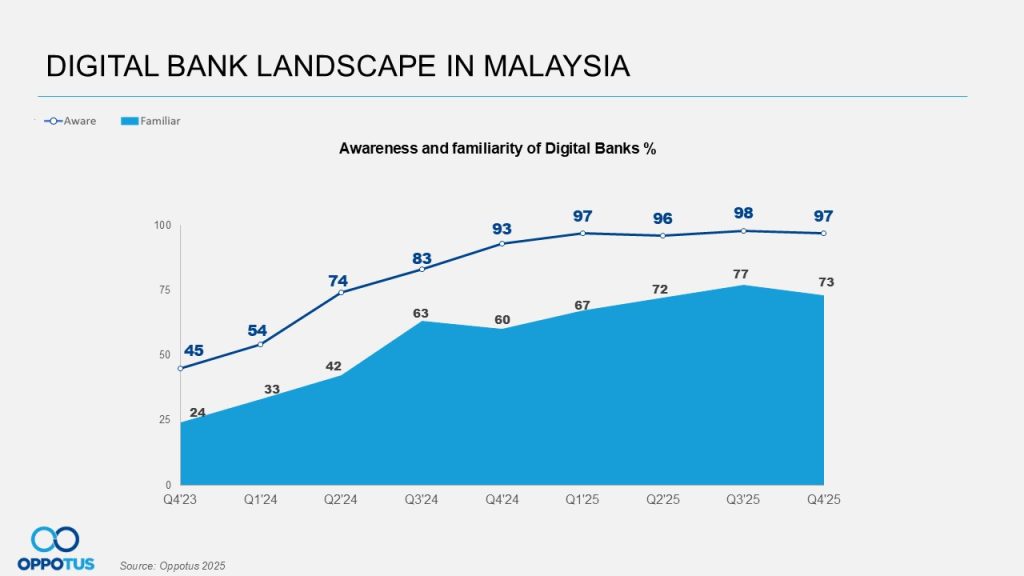

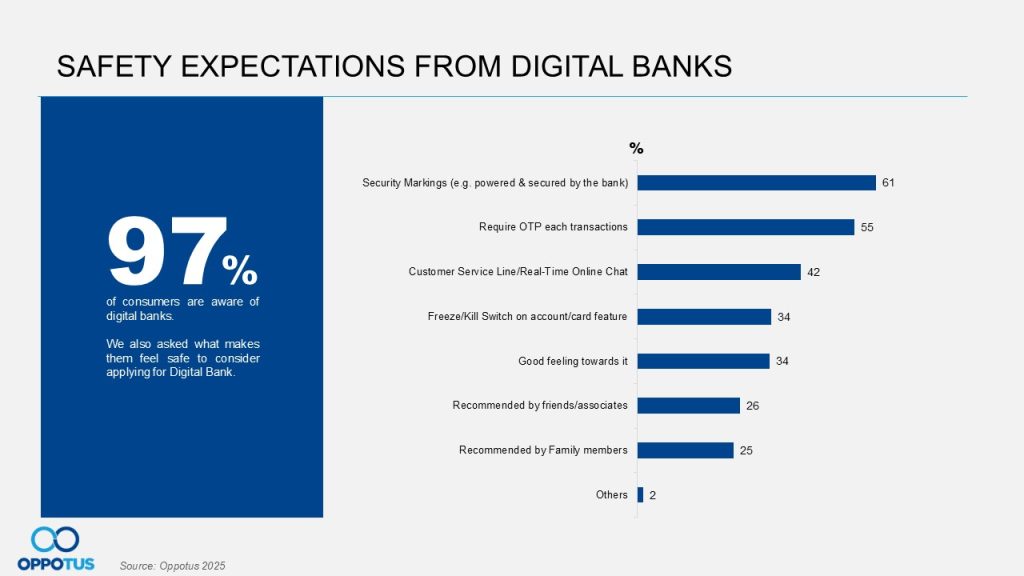

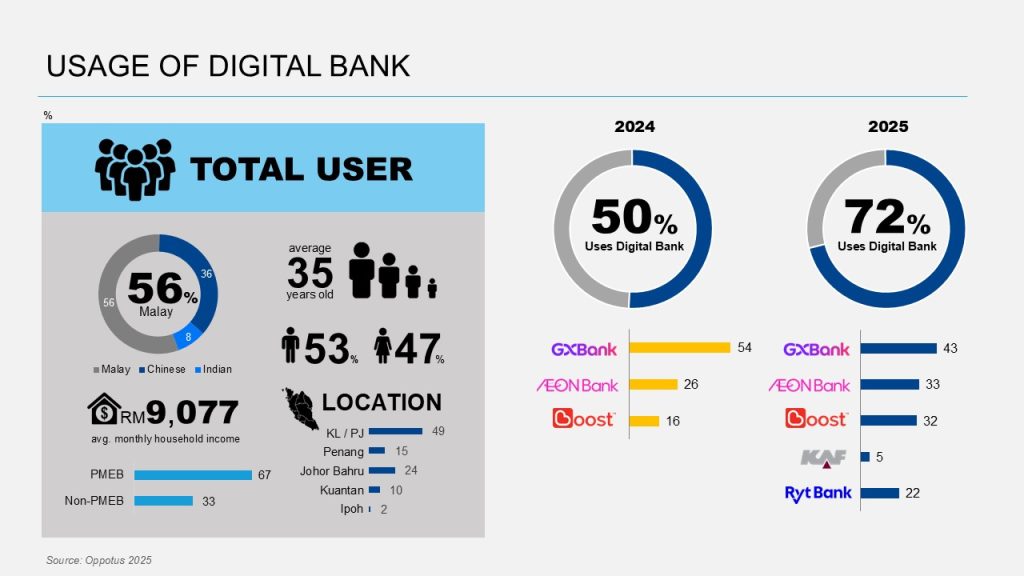

Since the start of digital bank, we have started measuring the awareness and familiarity of it amongst Malaysians at the end of 2023. We see that there has been a steady increase in both awareness and familiarity to the point that 97% of Malaysians were aware of them by the end of 2025, and more than 70% were familiar throughout most of 2025.

One possible factor that may be hindering the popularity of digital banks amongst Malaysians is the concern that they may not be as safe to store your money as conventional banks. When asked about what safety features would make them consider applying for a digital bank, the most common responses were for security markings, and for each transaction to require an OTP. A reliable customer service line/real-time only chat was also a relatively requested feature at 42%. It’s also notable that all of these potential security features were held in higher regard by Malaysians than being recommended by friends and/or family members, showing that Malaysians are much more concerned over tangible and proven security features than the supposed popularity of digital banks.

As of now, we have reached the point that the majority of respondents are using a digital bank in some form, with a 72% usage rate in 2025 compared to just 50% in 2024. GX Bank remains the most popular digital bank in Malaysia, although it no longer holds the majority share of usage, with more users opening accounts with Aeon Bank, Boost, KAF, and Ryt Bank. We also see that usage of digital banks is skewed mostly towards Malay and PMEB users.

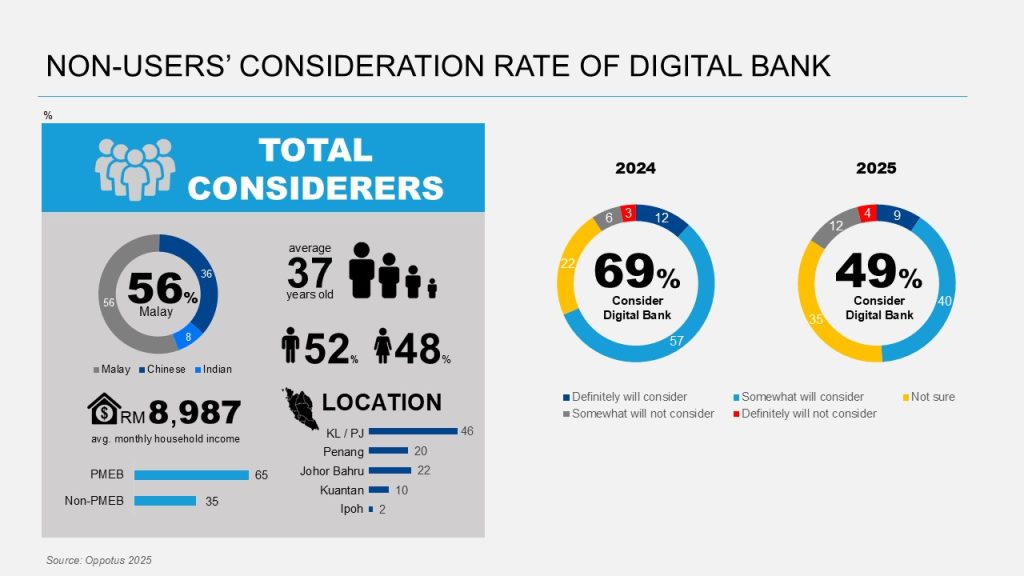

As for non-users, only 49% of those who don’t already use a digital bank in 2025 said that they would consider using a digital bank to some degree. This is down quite a bit from 2024 where 69% said they would consider a digital bank, but this could be due to a number of those respondents already making the jump to using a digital bank, leaving behind fewer respondents who aren’t already using digital banks with a larger proportion of people who are resistant to the idea of digital banks for various reasons such as security concerns.

Finally, we asked these respondents for the reasons why they would or wouldn’t consider using digital banks. For those who would consider digital banks, common reasons included the lack of need for branch visits, lower bank fees/charges, 24-hour accessibility and high interest rates. When it came to reasons people wouldn’t consider digital banks, security was the major concern, which is understandable since digital banks are a relatively new concept and the lack of a physical branch means that digital banks cannot offer the assurance of in-person assistance should users face any problems.

From this round of data, we see that Malaysia’s financial landscape is clearly moving toward a more digital and cashless future in 2026. More Malaysians are using e-wallets and those who do are spending more on a monthly basis than ever, demonstrating that Malaysians are increasingly comfortable with digital payment methods for everyday transactions. E-wallets have already established themselves as a core part of daily transactions for Malaysians, even surpassing cash as the most commonly used payment method for physical transactions.

Digital banks are also gaining traction at a notable pace. Awareness and familiarity among Malaysians are already high, and usage has grown significantly within a short period of time. Attractive benefits such as convenience, lower fees, and competitive interest rates continue to draw users toward digital banking services. However, concerns around security and the lack of physical branches remain key barriers preventing some consumers from fully embracing them.

How effectively will providers address these concerns while continuing to offer compelling value to users? As trust builds and security features become more transparent and robust, digital banks may increasingly complement or even compete with traditional banks the way e-wallets have come to stand by the side with cash transactions in everyday life for Malaysians. If you’d like to dive deeper into the data surrounding e-wallets and digital banks, feel free to contact us at theteam@oppotus.com